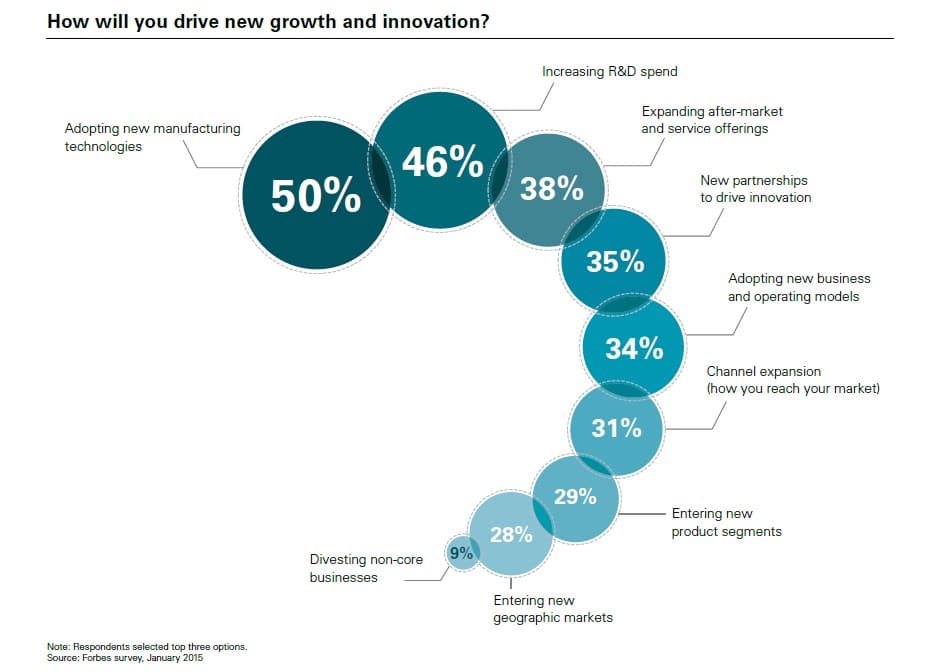

50% of A&D manufacturers expect new manufacturing technologies to drive future growth and innovation.

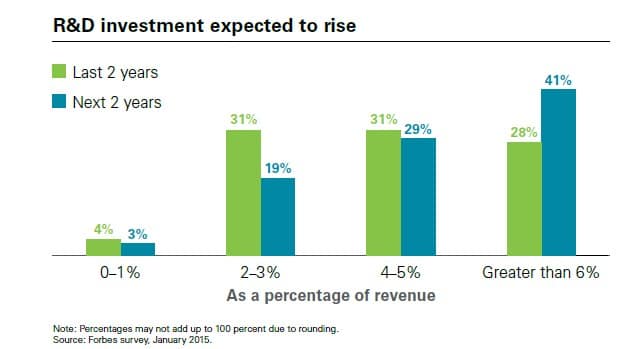

50% of A&D manufacturers expect new manufacturing technologies to drive future growth and innovation.- 41% of A&D manufacturers are forecasting their R&D spending will be greater than 6% of revenue in two years.

- Only 10% of A&D manufacturers said they have complete visibility of their supply chain operations, with 40% admitting they had only partial or limited visibility.

These and many other insights are from the KPMG Global Aerospace and Defense Outlook 2015 published last month. You can download a copy of the report here (free, no opt-in, PDF). KPMG’s research team found that A&D manufacturers are challenged to find the best opportunities for growth while balancing the time constraints, costs and risks of changing business models and increasingly complex supply chains. Please see page 18 of the study for an overview of the methodology.

Key take-aways from the report include the following:

- 50% of manufacturers are adopting new manufacturing technologies to drive new growth and innovation. Increasing R&D spend (46%), expanding after-market and service offerings (38%) and development new partnerships to drive innovation (35%) are also the most-often mentioned strategies A&D manufacturers are relying on to drive new growth and innovation. 34% are adopting new business and operating models, which is forcing an entirely new level of technology investment as well.

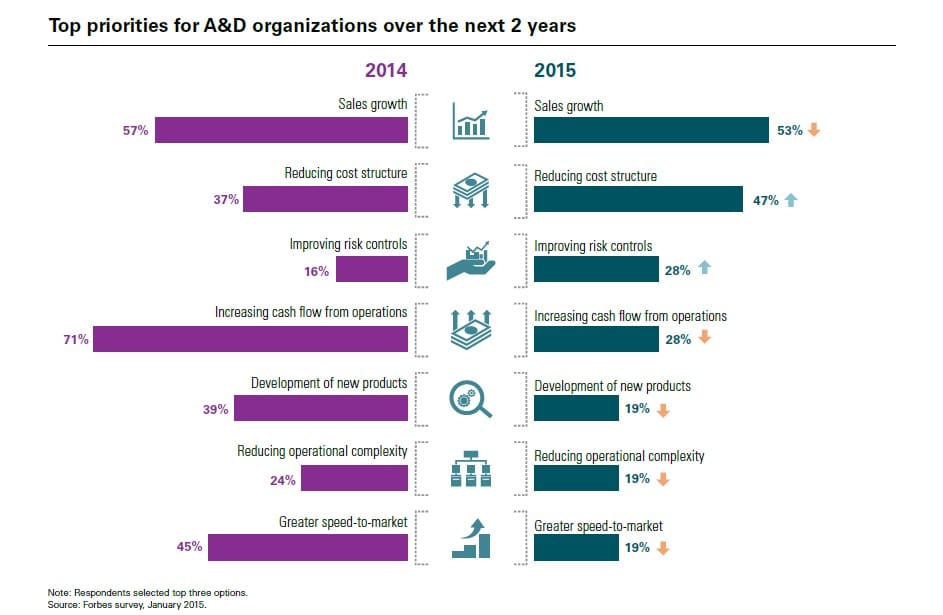

- Sales growth (53%), reducing cost structure (47%), improving risk controls (28%) and increasing cash flow from operations (28%) are the top three priorities for A&D manufacturers in 2015. Reducing cost structures and improving risk controls are trending up in the forecast period of the study. KPMG’s research team found that A&D manufacturers are striving to launch new business models while minimizing risk and controlling costs.

- Keeping their business models competitive (38%), efficiency in research and development/product development (32%), and intense competition and pressure on prices (26%) are the top three challenges facing A&D manufacturers. The research study also found that price volatility on key cost inputs (22%) and IT systems keeping pace with the demand from the business (21%) are the fourth and fifth most-mentioned challenges by A&D organizations. The following graphic provides an overview of the top five challenges A&D organizations face today:

- A&D manufacturers are projected to increase their R&D spending significantly in the next two years. 41% are forecasting their R&D spending will be greater than 6% of revenue in two years. 29% expect to invest between 4 and 5% of their revenue in R&D in the next two years. A comparison of R&D spending as a percentage of revenue is shown below.

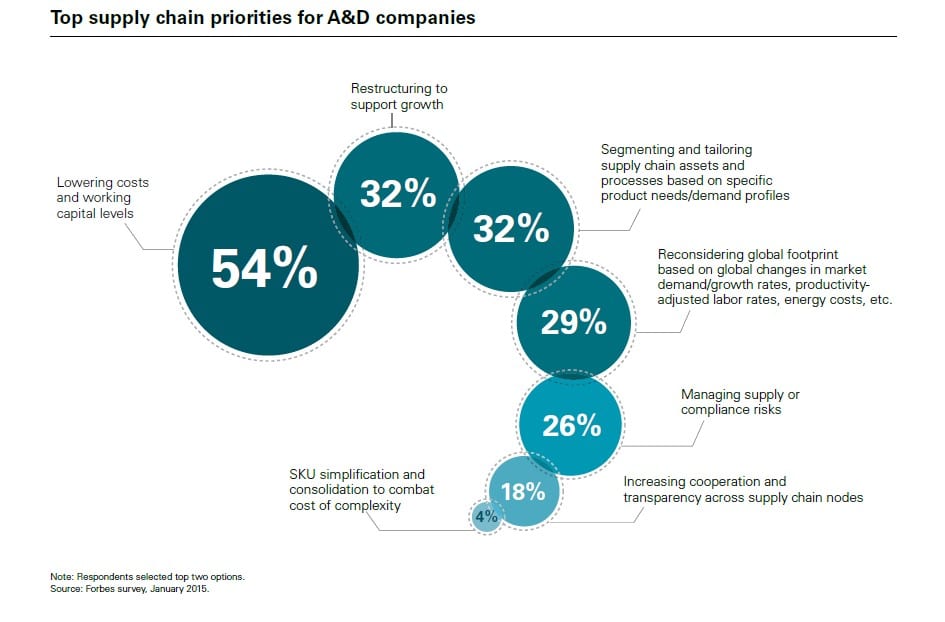

- Lowering costs and working capital levels (54%), restructuring to support growth (32%) and segmenting and tailoring supply chain assets and processes based on specific product needs/demand practices (32%) are the top three supply chain priorities. A&D manufacturers are concentrating on how they can attain more effective supply chain segmentation that can scale globally while reducing supply and compliance risks. These needs are a strong catalyst for future investment in technologies as more A&D manufacturers seek to optimize their supply chains by reducing costs and restructuring them to support growth.

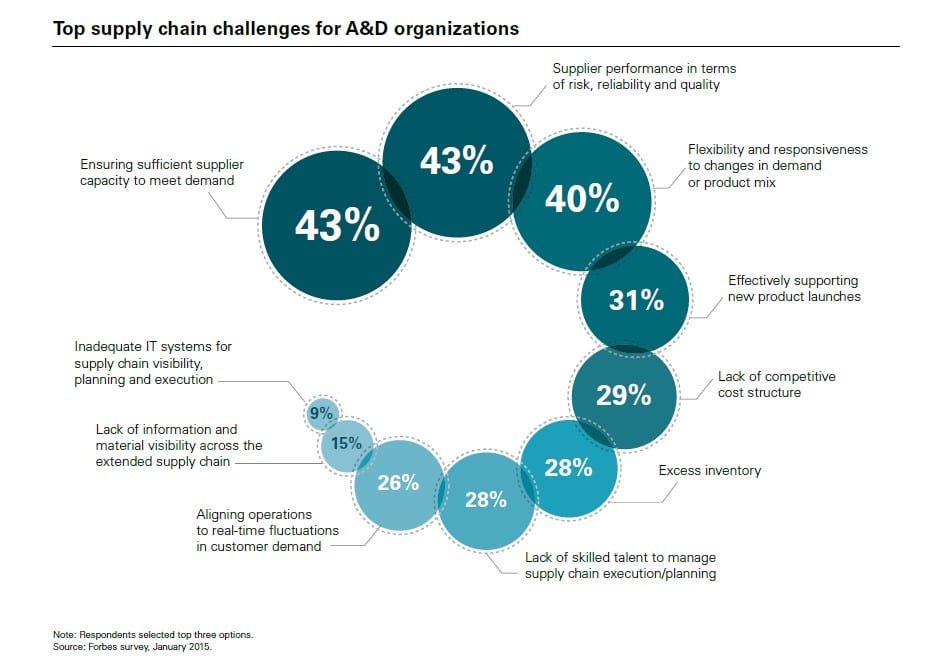

- The greatest supply chain challenges A&D manufacturers face include ensuring sufficient supplier capacity meet demand (43%), supplier performance in terms of risk, reliability and quality (43%) and flexibility and responsiveness to changes in demand or product mix (40%). The following graphic provides an overview of the top supply chain challenges faced: