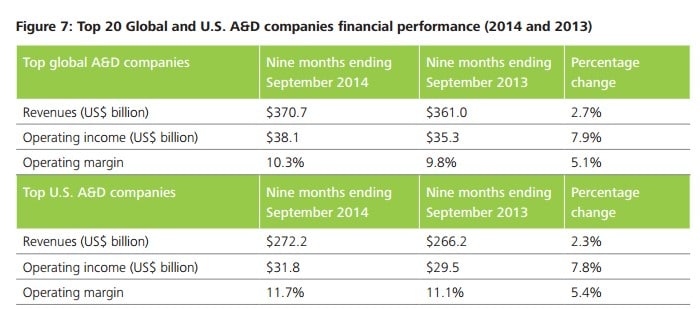

The top 20 U.S. A&D companies generated consistently higher gross margins (11.7% versus 10.3%) in the first nine months of 2014, and higher margin growth (5.4% versus 5.1%) compared to the top 20 global A&D companies.

The top 20 U.S. A&D companies generated consistently higher gross margins (11.7% versus 10.3%) in the first nine months of 2014, and higher margin growth (5.4% versus 5.1%) compared to the top 20 global A&D companies.

- Fuel costs, as a percentage of total operating costs for airlines have risen from an average of 13.6% in 2001 to 28.6% in 2014.

- The global Aerospace and Defense (A&D) industry is expected to grow at a 3% growth rate through 2015.

These and other key take-aways are from the 2015 Global Aerospace And Defense Industry Outlook published by Deloitte Touche Tohmatsu Limited (Deloitte Global) last month. You can download the report here (free, no opt in). Deloitte predicts the commercial aerospace sector will experience significant revenue and earnings growth in 2015 driven by record production levels at the platform and supplier base levels of the industry’s value chain. Deloitte is also seeing increased product rates due to accelerated replacement cycles of obsolete aircraft with more fuel-efficient models.

Key take-aways include the following:

- During the first nine months of 2014, the top 20 global A&D companies outperformed the top 20 U.S. A&D companies both in terms of revenue and operating income growth. The top 20 U.S. A&D companies outperformed their global counterparts on gross margin performance and growth. During the trailing nine months ending September 2014, the top 20 global A&D companies accounted for 52.3% of the industry revenues of US $709.4B reported in 2013. The top 20 U.S. A&D companies generated consistently higher gross margins (11.7% versus 10.3%) in the first nine months of 2014, and higher margin growth (5.4% versus 5.1%). The second graphic compares revenues and operating profits for the top global and U.S. A&D companies.

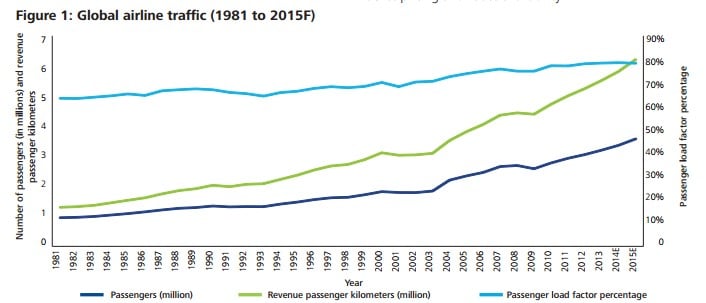

- Deloitte found that passenger travel demand increased 428% from 1981 to 2014E, while load factors (utilization of aircraft) have risen 25.4% (from 63.7% to 79.9%) during that same period. Deloitte also found the number of people flying per year continues to increase, with a 340% increase over that time, which is enabled by more affordable ticket pricing and route availability. The following figure shows industry growth from 2018 to estimate 2015 levels.

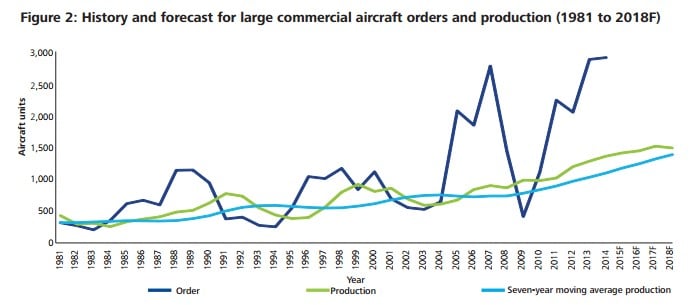

- Sales order and production history of commercial aircraft grew significantly from 1981 through 2014, generating a 218% increase in production between 1981 and 2014. Using a seven-year moving average, production levels over the last 20 years have increased 86.7% since 1994.

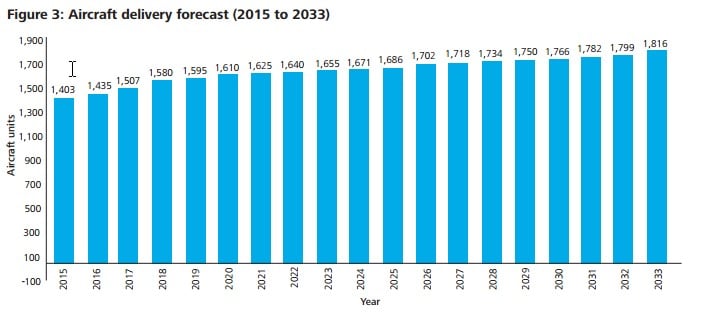

- Using Airbus, Boeing and industry forecast data, Deloitte predicts that over the next decade by 2025 commercial aircraft annual production levels are anticipated to increase by an estimated 20% or more. The following graphic illustrates their forecast through 2033.

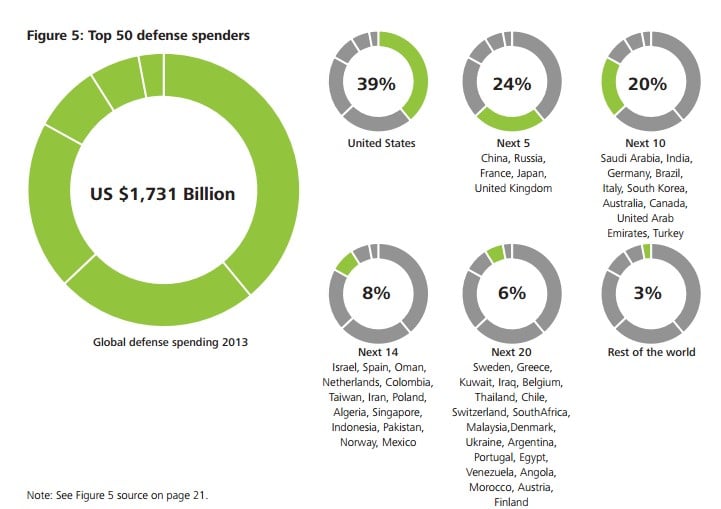

- The U.S. government continues to lead the world in defense spending with 39% of total global military spending. The following graphic compares national spending across the top 50 nations worldwide.

- Deloitte found that defense contractors continue to experience the effects of sequestration and are expected to for the foreseeable future. Their analysis found that in 2013, the top 20 U.S. defense contractors experienced a 2.5% reduction in revenues. The study notes that in the first nine months of 2014, the top 20 U.S. defense contractors have experienced a revenue decline of 2.1%, a trend expected to continue through the end of 2014.

- Fuel costs, as a percentage of total operating costs for airlines have risen from an average of 13.6% in 2001 to 28.6% in 2014.