Commercial aerospace sector orders grew from 2,858 in 2013 to record levels of 2,888 sales orders in 2014, while aircraft deliveries increased by 6.1% from 1,274 to 1,352 deliveries.

Commercial aerospace sector orders grew from 2,858 in 2013 to record levels of 2,888 sales orders in 2014, while aircraft deliveries increased by 6.1% from 1,274 to 1,352 deliveries.

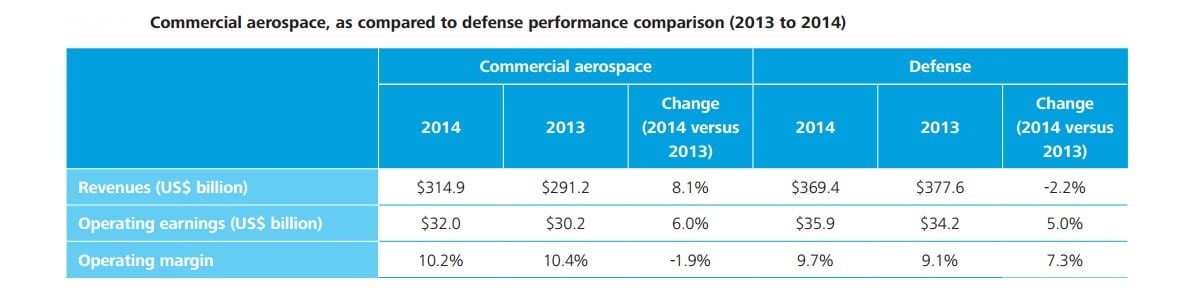

- Commercial aerospace subsector revenues increased by $23.6B in 2014, an 8.2% increase over 2013.

- Demand for new commercial aircraft is estimated to reach 34,000 jets over the next 20 years, with a value of over $1.78T at list prices

- Operating margins have been improving in the Aerospace and Defense (A&D) sector; 8.4% in 2012, 9.6% in 2013 and 9.8% growth in 2014.

- The Boeing Company and Airbus Group together added $6.1B in additional revenue in 2014, as a follow up to the $11B of combined incremental growth in 2013.

These and many other key insights are from the Deloitte’s 2015 Global Aerospace and Defense Sector Financial Performance Study: Growth Slowing, Profits Improving study (free, no opt-in) published in June of this year. Please see page 41 of the study for a definition of the methodology.

These and many other key insights are from the Deloitte’s 2015 Global Aerospace and Defense Sector Financial Performance Study: Growth Slowing, Profits Improving study (free, no opt-in) published in June of this year. Please see page 41 of the study for a definition of the methodology.

Key take-aways include the following:

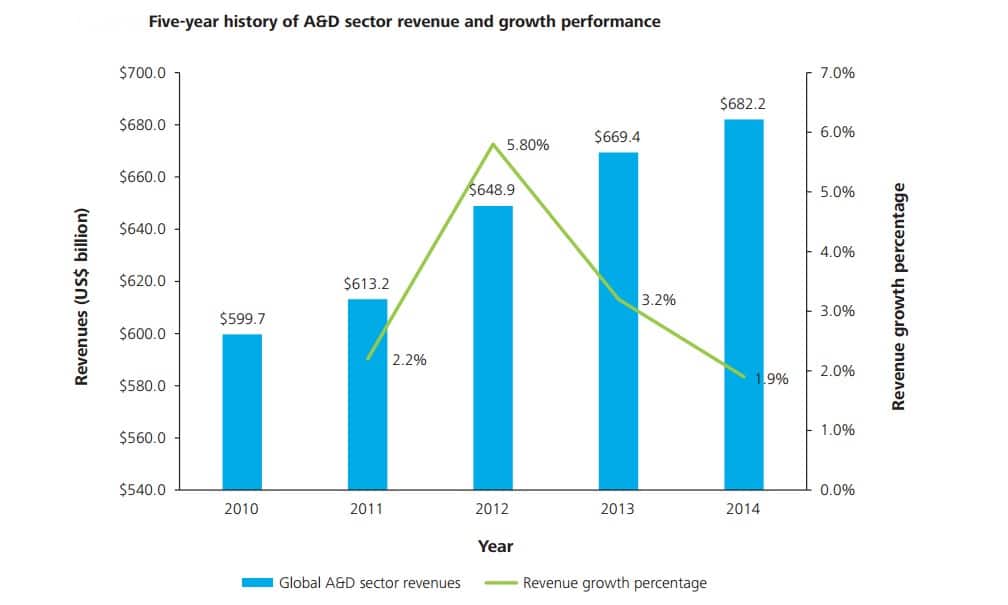

- Global Aerospace and Defense revenues grew 1.9% to $682.2B in 2014 from $669.4B in 2013. Deloitte found that record commercial aircraft production led by strong revenue growth at The Boeing Company and Airbus Group is the primary catalyst of revenue growth during the last two years. Although the global A&D sector added $12.7B to sector revenue, revenue growth rate declined in 2014, from 3.2% to 1.9%.

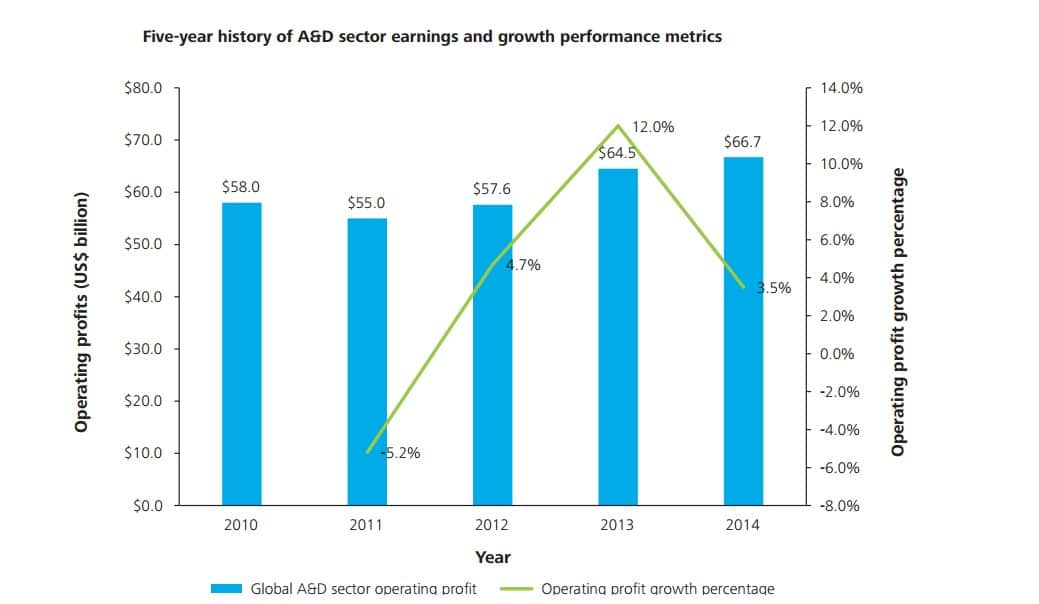

- Aerospace and Defense sector earnings outpaced revenue growth globally, adding approximately $2.2B in global profits. In 2014, the A&D sector’s operating earnings increased 3.5% to $66.7B in 2014. Deloitte attributed this to strong profit growth, especially among commercial aircraft manufacturers and propulsion equipment manufacturers.

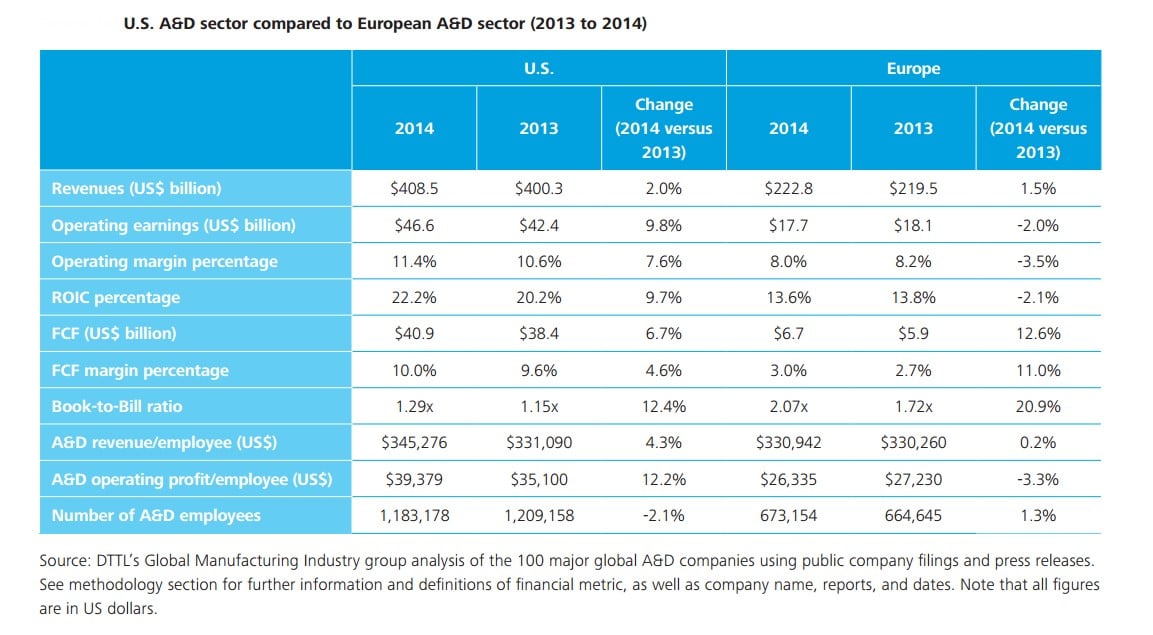

- S-based A&D companies accounted for 59.9% of the global A&D sector revenues, or $408.5B of the global A&D sector’s $682.2B revenues. European companies accounted for 32.7% or $222.8B of A&D sector revenues, while companies based in Japan, Canada, Brazil, and other countries generated the balance. In 2014, U.S. companies’ revenue increased 2.0%, while European companies’ revenue grew 1.5%. The table below provides a comparative analysis of revenue, earnings, Return on Invested Capital (ROIC) and key financial metrics.

- Deloitte found that the global commercial aerospace subsector grew 8.2%, with 78 more large commercial aircraft delivered in 2014 compared to 2013. Continuing the previous year’s pace, the commercial aerospace market attained the highest production level in its history. The Boeing Company and Airbus Group alone added $6.1B in additional revenue in 2014. The following table is a comparative analysis of commercial aerospace and defense spending.